5 Steps to Prepare Your Business for Unexpected Events: preparing business for unexpected events

Your top salesperson gives notice on a Friday. A key supplier shutters overnight. The lights stay off after a spring storm knocks out power across town. Revenue halts. Payroll doesn’t. Stress surges. Most small firms feel this gap before they see it. Preparing business for unexpected events is how you close that gap before it opens. Think of it as practical emergency preparedness that builds business resilience.

The playbook is practical, not theoretical: find the weak points that would hurt you tomorrow, build a modest cash cushion, document the few processes that keep the doors open, spread your dependency across more customers and suppliers, and check your insurance with fresh eyes once a year. This is risk management you can act on. That’s the spine of resilience. The details below make it real.

1) Identifying Common Business Risks

Start with five risks that consistently trip up small and mid-sized firms: key person dependency, cash flow crises, supplier disruption, customer concentration, and technology failures. Think of them as five dominoes arranged too closely. One falls, the rest wobble.

Key person dependency is simple to diagnose. If one person’s sick day becomes a company‑wide slowdown, you have it. The risk compounds when customer relationships, quoting, scheduling, or payroll sit in one head instead of in a shared system. A quick self-test: list your three most critical recurring tasks and circle the ones only one person can do. More than one circle is trouble.

Cash flow crises often arrive quietly and then all at once. Canadian survey data continue to show cost pressures and price shocks pushing firms to the edge. In the Canadian Survey on Business Conditions for Q2 2025, more than three-fifths of businesses expected cost‑related obstacles over the next quarter, with material costs jumping as a top concern. That’s not an abstract statistic; it shows up as squeezed gross margins and late supplier payments. The point is direct: when costs jump, liquid cash buys time. Statistics Canada’s CSBC release provides the broader picture of obstacles and rising input costs. (www150.statcan.gc.ca)

Supplier disruption is the external twin of cash strain. Even without a global crisis, localized bottlenecks, tariffs, or logistics delays can stop production. Many Canadian firms reported persistent supply chain challenges during and after the pandemic, and trade frictions in 2025 raised concerns about input costs and availability. That exposure shows why single‑supplier reliance is a structural risk, not just a procurement choice. See the CSBC detail and tariff‑exposure data for context. (www150.statcan.gc.ca)

Customer concentration is quieter but just as dangerous. If one client represents a third of your revenue, you’re effectively betting your payroll on their budget meeting. Lose them, and you’re sprinting to replace both revenue and receivables. Owners often rationalize this with “they always pay” until a merger, policy shift, or new procurement head changes the rules with one email. Want a directional gut check? If losing your largest customer would force immediate layoffs, your concentration is too high. For practical ways to map real rivals for those replacement customers, use a simple competitor field guide like How to Identify Your Real Competitors (Not Who You Think They Are).

Technology failures aren’t only about hackers. They include lost laptops, corrupted data, and a single point of failure in your point‑of‑sale system. But cyber risk deserves special mention. Statistics Canada’s 2023 cybercrime survey found about one in six Canadian businesses was hit by a cybersecurity incident, and Canada’s national cyber authority flags ransomware as a top threat in 2025 to 2027. For a small firm, that can mean days of downtime and reputation damage. The takeaway: technology is a risk vector, not just a tool. See StatsCan’s 2023 Impact of Cybercrime on Canadian Businesses and the Canadian Centre for Cyber Security’s ransomware outlook for why response plans matter. (www150.statcan.gc.ca, cyber.gc.ca)

So the risk is real. What can you do about it this month?

2) Actionable Steps to Mitigate Each Risk

You don’t need a 90‑page binder to get safer. You need a shortlist of moves you can complete in the next 30 days. Here’s how to reduce exposure on each of the five risks.

Key person dependency: This week, document the top three processes that keep revenue flowing. For many firms, that’s quoting, scheduling/fulfillment, and invoicing. Write them as simple checklists anyone competent can follow. Store them in a shared drive, and record a 10‑minute screen‑capture for each. Appoint a backup for each process and have them run it once end‑to‑end. Before: only Maya knows how to generate quotes from your custom spreadsheet. After: a two‑page checklist and a 6‑minute video let any trained coordinator produce accurate quotes in under 15 minutes. See the difference?

Cash flow crises: Adopt a 13‑week rolling cash flow and refresh it every Monday. It’s not a spreadsheet for accountants; it’s an early‑warning radar for owners. If the forward view shows a gap in week nine, you still have eight weeks to trim expenses, pull a promo forward, or negotiate terms. The Business Development Bank of Canada explains this approach clearly and why a weekly 13‑week window improves visibility when conditions change. (bdc.ca)

Supplier disruption: Create a “Plan B” supplier list for your top five SKUs or inputs. Start by asking current partners who they trust as alternates, check regional options, and pre‑vet one secondary supplier per key item. Negotiate skeleton terms now, even if you never place an order. It’s like keeping a spare tire in the trunk; you hope to ignore it for years, then it saves your quarter. For categories where tariffs or cross‑border friction are rising, ask domestic options to quote a “ready‑to‑ship in 72 hours” scenario so you know the premium for speed ahead of time.

Customer concentration: Install a simple revenue‑mix rule for the next 12 months: no single customer should account for more than 20 to 25% of trailing‑twelve‑month sales. If one does, design a mini‑campaign to add two midsized accounts in adjacent niches. One approach is to reverse‑engineer competitors’ messaging and offers. If you need a starting framework, use a lightweight SWOT to clarify what edge you can credibly claim today, not in a year. A practical template lives in How to Do a Competitor SWOT Analysis for Your Small Business. And if pricing strategy is the lever to attract those new accounts, borrow low‑cost tracking ideas from How to Track Competitor Pricing and Marketing Without Expensive Tools.

Technology failures: Do a two‑hour “resilience sprint” with your team. First hour: inventory critical systems (POS, accounting, CRM, cloud storage) and identify single points of failure. Second hour: implement one improvement per system. Enable MFA, set up daily backups, print a paper version of your incident contacts, and test a restore on one file. Government data show incidents are common, and national guidance underscores ransomware’s impact. Treat a tested backup like a fire extinguisher you know how to use. StatsCan’s cyber impact release and the Cyber Centre’s ransomware outlook explain why this matters. (www150.statcan.gc.ca, cyber.gc.ca)

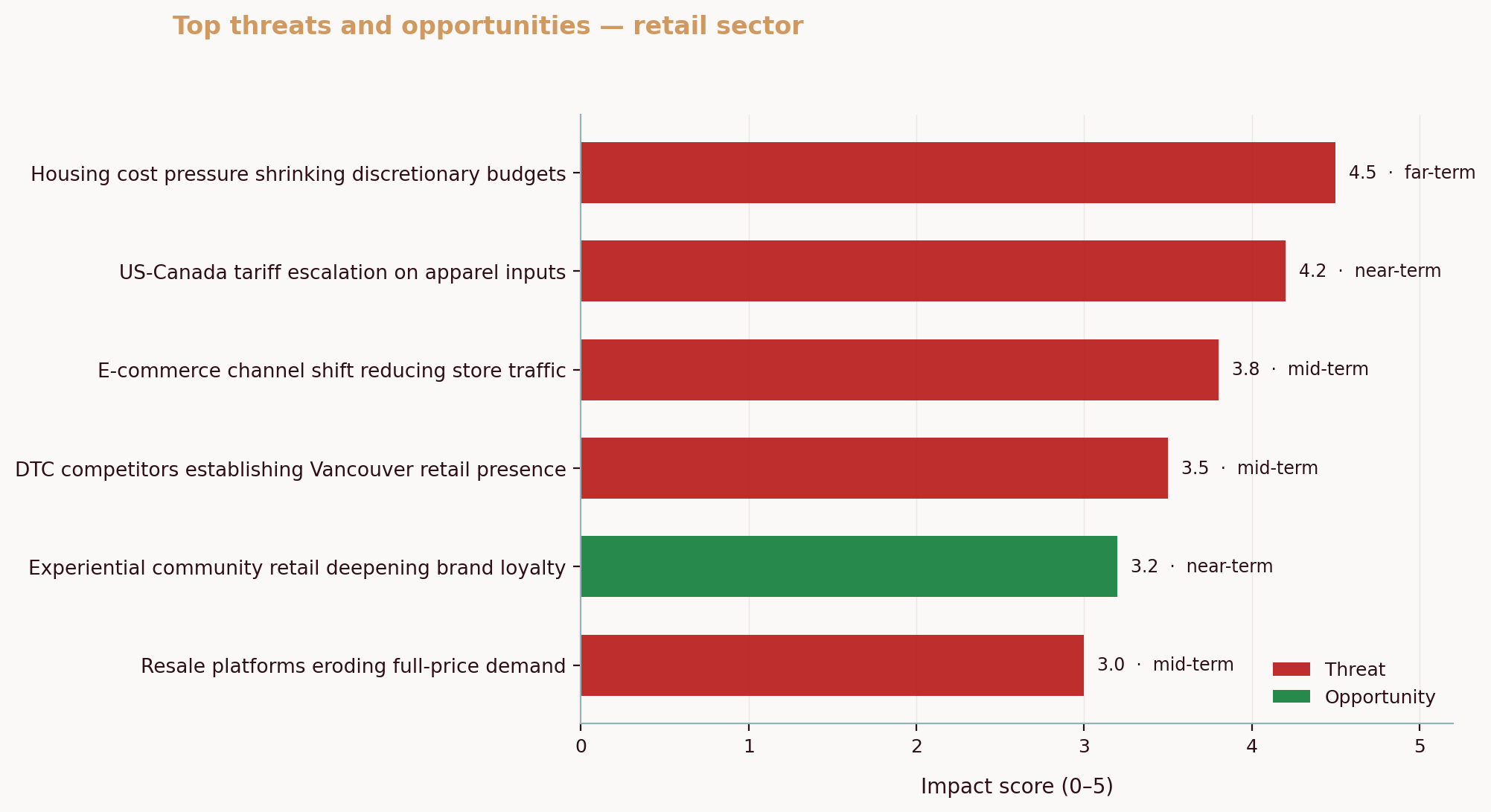

Real‑world signals reinforce these moves. In our March 2026 intelligence work, the Aurevon Intelligence Service saw two telling patterns: in Calgary’s custom metal fabrication niche, review scores were so saturated at the top that visibility, localized supply chains, and tech adoption (like CNC automation) determined wins; in Vancouver athletic wear retail, one brand’s 40% share of social mentions was eroding as new entrants and influencer‑led upstarts chipped away from multiple directions. Translation for risk planning: don’t anchor your fate to one channel or one partner when the battleground is shifting under your feet.

💡 Pro Tip

Write “how we do it here” for the three processes that generate or collect cash (for many, that’s quoting, fulfillment, and invoicing). Then schedule a 30‑minute handoff with a backup for each. This single habit slashes key person risk and shortens training for new hires.

Prefer to move even faster? Borrow this 7‑day mini‑sprint:

- Day 1: Build your 13‑week cash view and flag red weeks.

- Day 2: List top five SKUs/inputs and add one backup supplier contact for each.

- Day 3: Document one revenue‑critical process and record a screen‑share.

- Day 4: Enable MFA everywhere and test one file restore.

- Day 5: Rank customers by revenue share and set a 12‑month mix target.

- Day 6: Craft one outreach sequence for two adjacent‑niche prospects.

- Day 7: Draft a one‑page continuity checklist and share it with managers (that’s business continuity basics).

A quick analogy ties this sprint together: resilience is like diversifying your hiking gear. You pack a backup headlamp, extra water, and a map because trails change. Business trails do too. This is contingency planning in action.

3) Financial Preparation Strategies for Resilience

Money buys time to fix problems. That’s why simple finance moves matter.

Start with the three‑month cash reserve rule. As a rule of thumb for small firms in steady markets, holding at least three months of operating expenses in reserve, also called emergency savings, gives you breathing room to ride out a slow receivables month, an equipment failure, or a small sales slump. Some Canadian banking guides and SME resources recommend three to six months depending on volatility; the right number for you depends on seasonality, customer concentration, and access to credit. The concept of “cash runway” is the practical cousin of this rule and is easy to calculate. See the Business Development Bank of Canada’s plain‑language definition of a cash runway for a refresher. (bdc.ca)

Next, secure a line of credit before you need it. Lenders extend the best terms when your financials look healthy, not when you are in a pinch. Canadian guidance for entrepreneurs increasingly stresses this sequence: build the relationship early, match financing to use, and keep your operating line for working capital rather than long‑term assets. BDC’s advice on borrowing “before the economy takes a turn” captures the timing point clearly and highlights why a 13‑week cash view helps you decide sooner. (bdc.ca)

Then, review insurance annually. Treat it like a contract that needs to match today’s risk profile, not last year’s. If your revenue mix, equipment list, or supply chain footprint changed, your coverage may be misaligned. Put a date on the calendar each year to review property, interruption, cyber, and liability basics with your broker. The Insurance Bureau of Canada offers plain‑language guidance on core commercial coverages, including business interruption and cyber, which makes a handy pre‑meeting checklist. (ibc.ca)

Finally, accept that cash flow pain has been real for many Canadian SMEs, with many owners taking on fresh debt to manage obligations such as Canada Emergency Business Account (CEBA) repayment and higher input costs. That isn’t a reason to avoid a reserve; it is the reason to build one gradually. The Canadian Federation of Independent Business has documented how significant numbers of firms took on new debt to refinance CEBA in 2024, signaling tight liquidity. Use that as a nudge to start your reserve now, even if it grows slowly. (cfib-fcei.ca)

Here’s a compact way to compare the main financial moves:

| Strategy | Description | Timeline | Benefits |

|---|---|---|---|

| Three‑Month Cash Reserve | Hold at least three months of operating expenses in a dedicated reserve account. | Start this week; auto‑sweep 5–10% of monthly cash inflow until target reached. | Buys time during sales dips or delays; reduces panic decisions. |

| Line of Credit (LoC) | Pre‑approved operating credit tied to working capital needs. | Apply while financials are healthy; review limits annually. | Immediate liquidity for short‑term gaps; lower cost than emergency loans. |

| Annual Insurance Review | Adjust coverage to your current asset base, revenue mix, and risks. | Book a 60‑minute meeting once a year; add a mid‑year check after major changes. | Closes coverage gaps that could turn a disruption into a shutdown. |

| 13‑Week Cash Flow | Rolling weekly cash forecast with receipts and disbursements. | Build in one afternoon; refresh every Monday. | Early warning for cash crunches; sharper decision‑making. |

What does this mean for you? Pick one tactic to start today: open a separate reserve account and set an automatic transfer date on your calendar for the 1st of each month. Small transfers compound into real resilience.

4) Conducting a Stress Test for Your Business

A stress test is a short, pointed exercise that answers one question: if your biggest risk landed tomorrow, what actually breaks? It’s not a tabletop simulation with binders. It’s a focused walkthrough you can run in 90 minutes.

Step 1: Choose the risk to test. Use the five from Section 1 and pick the one with the most immediate impact. If you’re a contractor whose lead estimator handles both bids and vendor relationships, test key person dependency. If your POS and inventory tracking run on one laptop, test technology failure. If one client is 35% of revenue, test customer concentration.

Step 2: Frame a specific scenario and time box it to 72 hours. “Lead estimator is out for two weeks starting tomorrow.” Or “POS database corrupted on Saturday morning.” Or “Largest client pauses all orders for 60 days.” Narrow beats vague because it forces concrete decisions.

Step 3: Map the first 24, 48, and 72 hours. For each window, answer four prompts:

- Who needs to do what, in what order?

- What information, passwords, or files are required?

- What external calls or emails go out (customers, suppliers, bank, insurer)?

- What internal update goes to the team and how often?

Step 4: Identify single points of failure. If the backup signer for payroll is unclear, circle it. If vendor contacts live in one salesperson’s phone, circle it. If the only person who can reconcile the POS is on vacation, circle it.

Step 5: Assign tiny fixes with deadlines. Move supplier contacts into a shared CRM by Friday. Add a backup approver to payroll by Tuesday. Print a one‑page incident contact sheet and put it in the office emergency kit by Thursday. If a fix takes more than an hour, break it into a first step you can complete this week.

To make this vivid, imagine a Saskatoon sports bar on a busy playoff weekend. Diners want value, visible food safety, and an atmosphere worth leaving the couch for. That’s a triple pressure point on margins and operations. When a prep cook calls in sick and the keg order is delayed, the bar that mapped substitutions, cross‑trained staff, and pre‑arranged a local keg swap keeps the game on and the tabs open. The bar that didn’t starts turning guests away. Those pressures are not hypothetical; our March 2026 nightlife analysis surfaced exactly this three‑way squeeze on value, safety assurance, and atmosphere.

A second concrete example: a metal fabricator in Calgary faces a delayed overseas shipment. The shop with a vetted regional steel supplier pays a small premium but keeps jobs moving. The one without spends five days emailing brokers. In our March 2026 manufacturing research, visibility and localized supply chains separated winners from the pack. One decision upfront prevented a five‑figure production delay later.

If you sell into competitive consumer niches, add one more stress question: what happens if two new brands target your core audience with lower prices and influencer reach simultaneously? In 2026 Vancouver retail, that was not a theory; multi‑channel challengers were eroding share inside months, not years. Your stress test should include a “two‑front competitor attack,” then outline the offer and content you’d deploy in week one to hold share. To sharpen that plan, revisit your rival set with this field guide: Identify Your Real Competitors and refresh your SWOT with this template: Competitor SWOT for Small Business.

One last analogy: a stress test is like turning off your main breaker for five minutes to learn which lights actually matter. It’s controlled discomfort that reveals what to fix next.

Common Questions About Preparing for the Unexpected

What should I do first to prepare my business for unexpected events?

Start by naming the handful of risks that could stop revenue or collections tomorrow, then pick the biggest one. Today, document one revenue‑critical process (for many, quoting or invoicing) in a two‑page checklist and a short screen‑recording, store it in a shared drive, and ask a backup person to run it once. That single move reduces key person dependency and creates momentum for the rest of your business contingency planning. Asked another way, how do I protect my small business from risks? Begin with these basics: identify your top exposures, add simple backups and checklists, diversify suppliers and customers, and maintain cash and insurance buffers.

How much cash reserve should I maintain?

Aim for at least three months of operating expenses, and adjust upward if your revenue is seasonal or concentrated in a few clients. This is your emergency savings for the business. The concept of a cash runway, explained clearly by BDC, gives you a formula to check your cushion against burn rate. A weekly 13‑week cash forecast ties the target to reality by showing shortfalls early enough to act. (bdc.ca)

How often should I review my business continuity plan?

Once a year, plus after any material change such as adding a new product line, switching ERPs or POS, opening a new location, or crossing a revenue threshold that changes your insurance needs. Treat the review like a renewal meeting: confirm backups for critical roles, scan supplier and customer concentration, run a 60‑minute stress test on your top risk, and update contact sheets. For clarity, a business continuity plan is a short playbook that explains how you will keep essential operations running during and after a disruption, including roles, contacts, and recovery steps. It’s routine maintenance, like changing winter tires before the first storm. If you want a deeper dive on crisis planning tools, BDC’s overview includes a 13‑week cash‑flow planner you can use during disruptions. (bdc.ca)

What if I don’t have the resources to implement all these strategies?

You don’t need them all at once. Prioritize by impact and effort. Pair one “fast win” (document a process, enable MFA, create a backup supplier contact) with one “foundational move” (start the reserve with a small monthly auto‑transfer or apply for a modest line of credit). The pattern builds capacity over time. When cost pressures bite, remember that many Canadian SMEs have had to take on extra debt to manage obligations in recent years; a small reserve and pre‑approved credit are what keep a hiccup from becoming a crisis. (cfib-fcei.ca)

5) Conclusion and Next Steps

You don’t control storms, resignations, tariffs, or malware. You control whether a single surprise can stop your business. Start the flywheel today: run a 90‑minute stress test on your biggest risk, open a separate reserve account and set a monthly auto‑transfer, and book a 30‑minute team huddle to assign backups for quoting, fulfillment, and invoicing. Small steps compound.

Want one concrete, do‑it‑today action? Build your 13‑week cash view this afternoon and share it with your manager or bookkeeper. Then circle the first red week and write one move to pull it back into the black. That habit, more than any binder, is what keeps the doors open when the unexpected knocks.

A final thought: resilience is a choice you make while things are calm. Make it now.

If you want affordable, Canada‑specific market context to inform your planning cadence, Aurevon’s Ecosystem Dynamics Report distills competitor moves, channel shifts, and buyer signals into an actionable brief you can refresh quarterly. See how it supports contingency and “what if” planning for SMB owners at aurevon.ca/ecosystem-dynamics-report.

Mitchell Ozmun

SMB Researcher, Business Analyst - Saskatchewan Born and Raised