Vancouver Athletic Wear Retailers Face 2026 Market Erosion

Vancouver Athletic Wear Retailers Face 2026 Market Erosion

Shoppers scroll. Likes spike. Sales dip. The paradox is alive on the West Coast: a single retailer can dominate local buzz while watchable transactions slide to rivals. That gap is exactly where Vancouver athletic wear SMBs are losing share today, and it’s fixable if you combine three levers that big brands can’t copy fast: place-based authenticity, value-led pricing, and experience-first retail. In other words, win the athletic wear retail competition locally, not just the conversation.

Across Metro Vancouver, social chatter tilts heavily toward one athletic retailer, yet transactions continue to leak to national chains, influencer-fueled direct-to-consumer labels, and price-first marketplaces. Our March 2026 local-market read shows that social-mention dominance does not equal immunity from erosion when shoppers encounter aggressive promos from JD Sports Vancouver, the broad price entry of Decathlon Metro Vancouver, and aspirational DTC fashion disruption tied to Gen Z fashion trends. Awareness is loud. Wallets are quiet. That mismatch is where you win back ground in the metro vancouver retail landscape.

Current market signal: social-mention dominance vs. real share

Think of social mentions like a stadium cheer and share-of-wallet like the scoreboard. Loud doesn’t always mean leading. Mentions, impressions, and follower counts are awareness metrics, while sell-through, average unit retail (AUR), basket size, and repeat-rate are transactional. When SMB owners mistake the former for the latter, they overestimate resilience and underinvest in the levers that convert talk into paid orders. Put simply, social media brand dominance is a vanity signal unless you tie it to conversion.

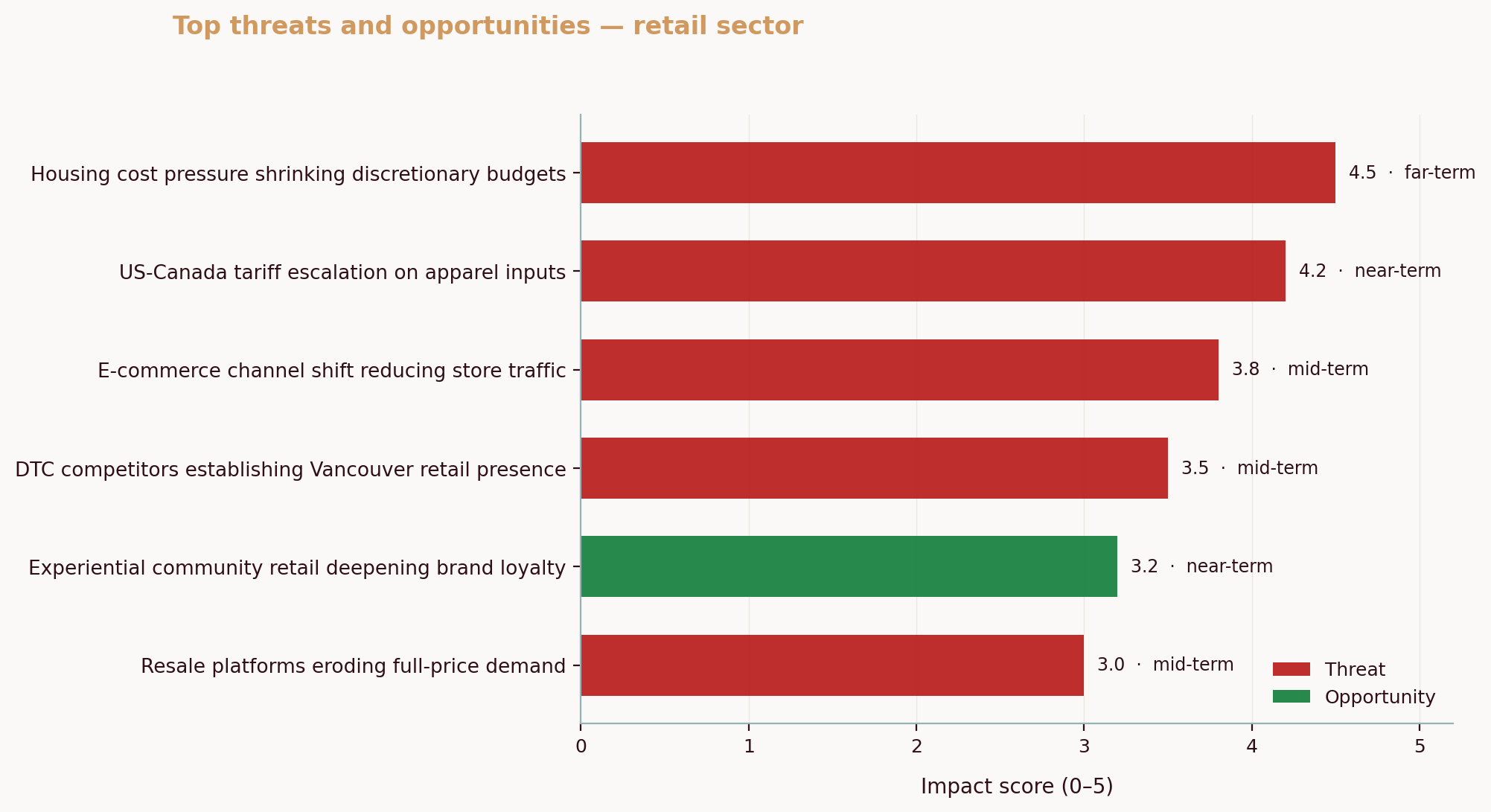

In March 2026, the Aurevon Intelligence Service reviewed Canadian retail SMBs and found a recurring pattern: social-mention peaks often coincide with campaign bursts, not with durable movement in basket or repeat purchasing. Across 5 Canadian retail SMBs analyzed via the Intelligence Service, median Google ratings sat at 4.6 with a p10–p90 range of 4.16–4.67, and the median review count reached 682. High reputation did not stop share shifts toward better-priced basics and omnichannel fulfillment. For context, national demand data also show consumers are budgeting tightly; the Bank of Canada’s Q2 2025 consumer expectations survey reported weaker discretionary spending intentions and rising pessimism about personal finances. That translates to stricter trade-offs in-store and online. Bank of Canada CSCE

If you already dominate local chatter, the next sections explain why share still leaks and how to close the gap.

Multi-front competitive landscape: JD Sports, Decathlon, and influencer brands

Three vectors pressure local SMBs at once. First, JD Sports runs national promotions and fast-turn drops that reset price expectations for brand-name footwear and apparel. Second, Decathlon’s wide, own-label assortment positions it as the value gateway for families and casual athletes. Third, influencer brands like Vuori and Alo Yoga convert glossy content into “I want it now” demand that siphons premium purchases, especially among younger shoppers. It’s like sending three different salespeople to pitch the same customer: one wins on price, one on breadth, one on aspiration. Asked who the biggest competitors are in this market, the shortest list is JD Sports, Decathlon, and content-led DTC labels such as Vuori and Alo Yoga.

Operationally, these rivals play different games. JD Sports blends omnichannel convenience with national buying power. Decathlon uses vertical product development to undercut third-party brands. DTC upstarts keep lean assortments and high storytelling intensity, converting social to site to cart in minutes. Sportswear influencer marketing compresses the path to purchase by turning discovery into intent with creator reviews, affiliate codes, and fit demos. Local retailers most often lose the transaction where price anchors get set (first search), where size or color availability breaks (assortment gaps), or when content-driven desire outpaces in-store experiences. National reports mirror this split dynamic: Deloitte’s 2025 outlook notes most Canadians still expect higher prices and are searching for value even during peak seasons, a sign that premium pricing backlash is real. Deloitte Canada holiday outlook

What does this mean for you? You can’t beat everyone at everything. You can exploit where they’re slow locally.

| Competitor | Strength (price/assortment/brand) | Primary channel advantage | Local SMB vulnerability | Tactical countermeasure |

|---|---|---|---|---|

| JD Sports | Price on marquee styles, hype timing | National promos, buy-online-pickup | Promo anchoring lowers perceived fair price | Introduce limited-run local collabs with “value floors,” and use competitor SWOT analysis to identify SKUs worth holding margin on |

| Decathlon | Assortment depth at entry prices | Vertical brands, wide formats | Lost entry-level baskets and family bundles | Build “starter kits” and local club bundles; track rivals through competitor pricing methods |

| Vuori/Alo (DTC) | Aspirational premium, content engine | Fast social-to-cart | Lost fashion-forward baskets | Run micro-drops with local creators and fit clinics; clarify real competitors via identify your real competitors |

Consumer price pushback and elasticities in local athletic apparel

Price resistance is highest where products feel interchangeable. In basics and lifestyle athleisure, elasticity is high; small price cuts move volume. In technical outerwear and performance baselayers, elasticity softens when fit and function are proven in-store. Vancouver shoppers weigh rain-ready performance and trail-to-city versatility, then decide whether brand aspiration justifies a premium. When rent and payments pinch, they don’t stop buying; they recalibrate. Premium pricing challenges show up when shoppers perceive little functional differentiation and when heavy promos reset reference prices.

Evidence backs this caution. Statistics Canada reported clothing-related sales growth into late 2025 even as households juggled budgets, suggesting consumers stayed active but hunted for value tiers and promos. Statistics Canada retail trade, Dec 2025 At the same time, real estate and retail trackers show a reset under way, with large amounts of space returning to market and food-led formats pulling foot traffic back to mixed-use districts. That shifts where discovery happens and which neighbors feed you spillover. Cushman & Wakefield 2026 guide

Why are consumers pushing back on premium pricing? Higher living costs, constant discounting that anchors price expectations, and the rise of direct-to-consumer disruption that offers close-enough quality at lower tickets. Analogy time: pricing a fleece jogger like it’s a technical shell is like charging concert prices for a sound check. The audience knows the difference.

March 2026 findings applied to local risk segments

Across 5 Canadian retail SMBs analyzed via the Aurevon Intelligence Service, three threat clusters appeared again and again: e‑commerce price undercutting (average impact 4.2), structural footfall decline (4.2), and macro pressure on discretionary spend (4.4). Tag analysis surfaced “experiential retail” and “athleisure” in 7 and 5 reports respectively, a sign that shoppers still respond to hands-on discovery when it feels local and useful. Review quality was strong (median 4.6), yet businesses with high ratings still lost share where value assortments were thin or events were sporadic.

Translating that to Vancouver risk cohorts:

- Value-seeking shoppers: defect when entry-price gaps exceed 10–15% on basics or when family bundles don’t exist. They respond to transparent tiered pricing and clear “good-better-best” walls. To map these competitors accurately, start with how to identify your real competitors.

- Occasion-driven buyers: swing to whoever solves a near-term need, like a trail race kit, at the right price. If your size run or fulfillment is shaky, they bounce. Strengthen monitoring with how to track competitor pricing.

- Aspirational but price-sensitive: love DTC storytelling yet won’t pay unlimited premiums. They convert when try-ons, fit advice, and small exclusives meet them in-store.

Trade risks also linger. Tariff and trade policy reset risks were flagged in 3 reports with high impact, echoing small business surveys about potential cost shocks that would raise landed costs for apparel. CFIB “Your Voice” Feb 2026 See the difference? Social strength without value tiers and local depth leaves exposed flanks across all three cohorts. The fix relies on disciplined retail pricing strategies linked to localized service.

Tactical strategies and implementation roadmap for SMBs

Here’s how this actually works on the floor.

Hyper-local assortment and micro-buys: Run 6–12 piece test-buys tied to neighborhood use cases like “sea-to-summit commute” or “rain-ready run club.” Label walls by activity and weather, not just by brand. It makes comparison easy and shifts decisions from “which logo” to “which fit for my routine.”

Tiered pricing and value bundles: Protect margin on premium, limited-run lifestyle items while creating clear entry SKUs. Bundle basics into “starter kits” for running, studio, or weekend hikes. Publish bundle savings in-store and in paid local search. If JD Sports anchors price on a marquee item, hold your ground on that style, then capture the rest of the basket with bundle value. For structure, lean on a quick competitor SWOT to rank SKUs by “match” or “differentiate.”

Experience-first programs: Co-host with studios and clubs. Offer 20-minute gait checks, “wash-and-care” clinics, or repair-and-rewear nights. Add a lightweight membership: early access to micro-drops, one free service per quarter, and a quarterly swap event for kids’ sizes. This turns social buzz into repeat visits and helps protect market share in athletic wear through useful touchpoints.

Targeted digital-local and fulfillment: Build 500–1,000 person CRM micro-segments by activity and price sensitivity. Push “back-in-stock” and “bundle only” offers to those groups. Use next-day local delivery on event weeks, and promise a two-hour “size find” service across your store or sister locations.

Before/after you can execute this month:

- Before: one big seasonal buy, static pricing, sporadic events. After: rolling micro-drops, A/B tested price ladders, weekly clinics tied to local calendars.

| Pilot name | Objective | Duration | Primary KPI | Estimated cost/risk |

|---|---|---|---|---|

| Value Bundle Sprint | Prove elasticity on basics | 30–45 days | Sell-through lift on bundle SKUs | Low inventory risk, moderate promo cost |

| Creator Micro-Drop | Drive premium sell-through without deep promos | 60 days | AUR on limited-run items | Low units, higher planning time |

| Fit & Fulfillment Blitz |

Mitchell Ozmun

SMB Researcher, Business Analyst - Saskatchewan Born and Raised