London construction suppliers can beat big-box rivals in 2026

Starts slip. Quotes go stale. Another contractor asks for an EPD-backed insulation you don’t stock. You lose the job. The pattern is familiar across the construction materials market London depends on: local housing starts have cooled while specification demand for sustainable, code‑compliant products climbs. CMHC’s latest reports show Ontario lagging in ground‑oriented homebuilding despite record completions in 2025, a mix that squeezes cash flow for smaller distributors and heightens the cost of slow inventory turns across the construction supply chain. That tension is exactly where independent specialists win. When contractors buy to spec, speed and certainty beat sticker price. London construction suppliers that pair specialty sustainable SKUs with BIM‑ready product data and targeted B2B e‑commerce can outpace big‑box rivals this year. CMHC Housing Supply Report, Spring 2026.

Related: 5 Things I Wish I Knew Before Starting a Construction Business — Jesse Lane

1. The market squeeze in London construction materials: what Aurevon’s analysis reveals

In March 2026, Aurevon Intelligence Service analysis of Canadian construction SMB dynamics highlighted a London‑specific bind: fewer local starts and tighter financing cycles collide with rising requests for certified, lower‑carbon products. CMHC’s monthly releases through late 2025 also recorded weaker year‑to‑date starts for London versus the prior year, a signal that volume‑led strategies will struggle to protect margins. These local housing market trends in the London Ontario construction market point to a pivot, inventory policy should shift toward higher‑margin, spec‑driven lines and specialty building materials. CMHC September 2025.

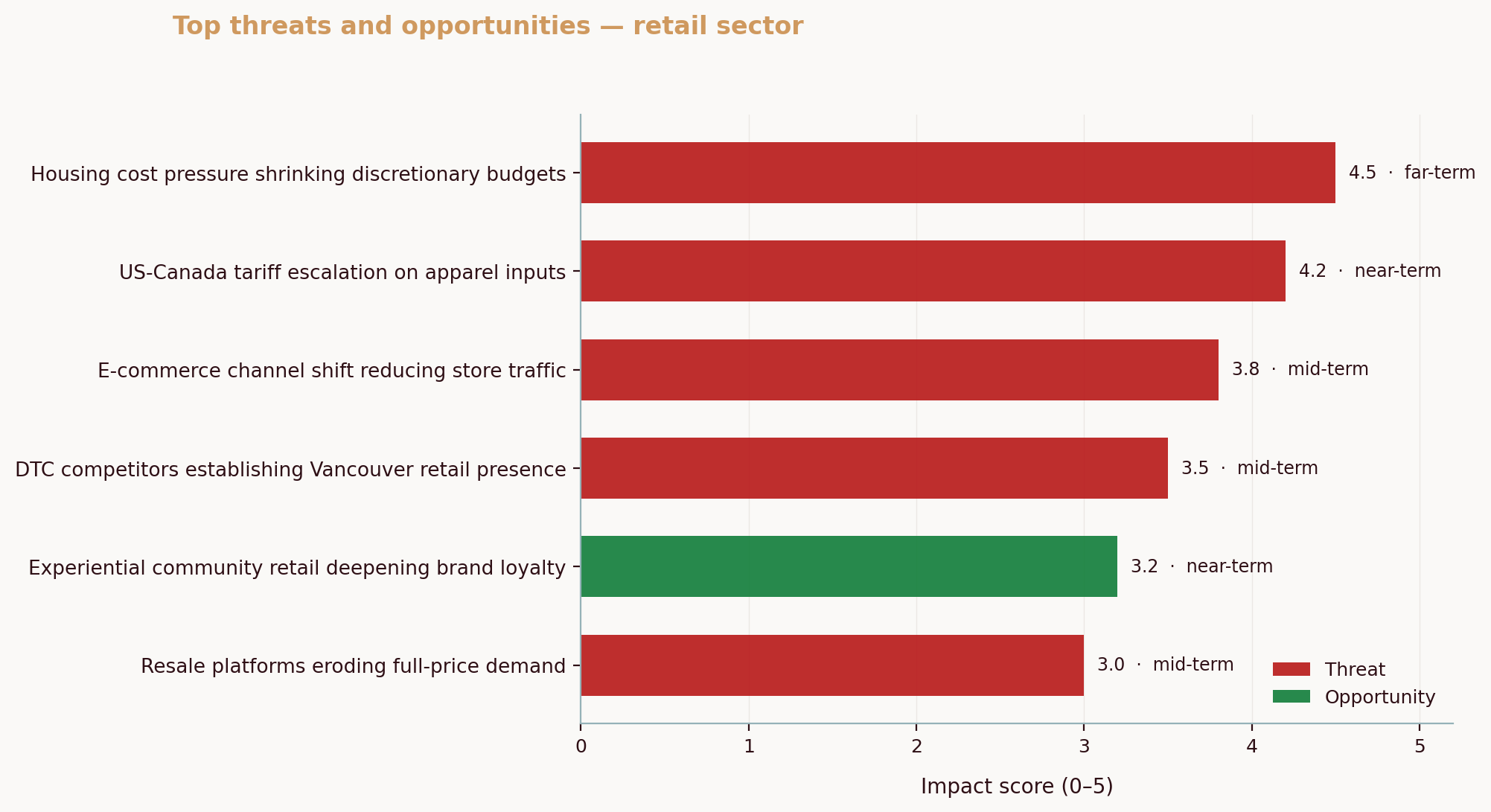

Across 5 Canadian retail business SMBs analyzed via the Aurevon Intelligence Service, e‑commerce price undercutting appears as a top recurring threat (avg impact 4.0), while sustainability is a consistent opportunity theme. Those patterns now surface in construction procurement too: online price hunting chips away at commodity margins, but green‑spec projects reward verified performance and documentation. Local firms feel it directly. Consider Copp’s Buildall, a London staple whose online catalogue signals a push to meet customers where they search; the takeaway isn’t their brand, it’s the behavior their site reflects: contractors expect digital clarity on availability, specs, and pickup or delivery. That expectation is your opening. Copp’s Buildall product catalogue.

If you’re unsure who you’re really competing with in each line, use a fast reset with how to identify your real competitors to map the digital and local players stealing orders today.

2. Why big-box retailers are vulnerable in this environment

National chains are built for breadth and price signaling. In a squeeze where designers and inspectors anchor decisions to code, certifications, and submittal packages, those strengths become friction. Centralized buying often delays local onboarding of a new fire‑rated assembly or low‑carbon concrete admixture. Assortments go wide but shallow, which hurts when a GC wants 120 identical units of a specific, certified SKU with matching EPDs (environmental product declarations). Product‑data updates lag, so BIM objects and spec sheets stay generic or missing, pushing risk back onto the contractor. When budgets tighten, nobody wants install surprises or re‑inspections. Certainty wins.

You can make that contrast explicit for your team and your customers. Independent building suppliers can compete with big‑box retail challenges by leaning into code compliance construction support, deeper depth in certified lines, and faster submittal turnaround.

| Consideration | Independent suppliers (advantages) | Big-box retailers (weaknesses) |

|---|---|---|

| SKU depth in specialty lines | Deeper stock in targeted certified products and accessories that pass local inspections | Broad catalogues, shallow depth in niche certified SKUs |

| Product data and submittals | Fast access to datasheets, EPDs, code references, install guides tied to SKUs | Fragmented or generic PDFs, slower updates |

| Local code agility | Direct relationships with local inspectors and designers, quick pivots when OBC references change | Centralized decisions slow response to local code or municipal program shifts |

| Delivery and kitting | Job‑pack kitting for spec assemblies, timed drops | Standard parcel or pallet flows, limited kitting |

| Decision support | Staff who know specs and failure modes | Price‑centric sales motions |

The City of London’s BetterHomes retrofit program and similar incentives raise homeowner demand for efficient materials, which increases the share of projects that buy to documentation. That tilts the field toward suppliers who can prove compliance, not just match price. City of London BetterHomes.

For more structure as you assess your position, pull a quick competitor SWOT analysis and keep it visible in your sales room.

3. Demand drivers: sustainability, code compliance and the rise of specification buying

Two forces set the tone in 2026. First, code and program alignment. Ontario’s 2024 Building Code reduces provincial‑national discrepancies and updates referenced standards, which tightens product expectations on jobs inspected this year. Second, more owners, lenders, and municipalities ask for traceable performance. Together, that pushes buyers to spec: they want the exact certified insulation, the exact window performance class, the exact VOC certificate, with documentation ready for submittals and closeout. If the vendor also offers install support, so much the better. Ontario 2024 Building Code.

What is driving demand for sustainable building materials in Canada? Three practical factors show up on London bids, incentives that reward efficient envelopes, code compliance construction requirements that reference updated standards, and client policies that prioritize lower‑carbon, sustainable building products with transparent EPDs.

What does this mean for you? Think of specification as a “pre‑sold cart.” When your product data lives in the model or spec, the PO follows the documentation. It’s like sending two salespeople to the same client: one shows up with signed drawings and sealed calcs, the other with a discount. The first wins most days.

Across 5 Canadian retail business SMBs analyzed via the Aurevon Intelligence Service, “Brand Trust and Reputation Risk” surfaced repeatedly: ratings and recalls move revenue quickly. Translate that to construction: if a submittal is rejected or an inspection fails, the cost dwarfs any small unit price gap. Public ratings, especially Google reviews, now sit upstream of many purchasing decisions and can amplify or erode local trust in days. That’s why specialty sustainable SKUs, paired with airtight datasheets and EPDs, often command higher margins and stickier contractor relationships.

A concrete before/after helps. Before: a generic “R‑22 batt” on the shelf, no EPD, no compatibility notes. After: a curated “Code‑Tier Pack” including R‑22 mineral wool with third‑party EPD, matching acoustic sealant, fasteners, install guide references, and a link to a downloadable BIM family. See the difference?

If you need to sanity‑check who’s really stealing these spec‑driven orders, revisit how to track competitor pricing and marketing and watch bid‑board mentions.

4. Digital threats and opportunities: B2B e‑commerce, BIM and product‑data integration

B2B e‑commerce is no longer experimental. McKinsey’s 2024 B2B Pulse found buyer comfort with high‑value remote and self‑serve orders surging, with digital now the cornerstone of growth. That matters even if you sell locally, because procurement teams expect an order portal, real‑time availability, and downloadable data. If your catalogue is invisible to search and your PDFs aren’t tied to SKUs, a national marketplace will intercept intent before your counter staff ever hears the question. This is where B2B e‑commerce for construction, tied to clean product data, compounds advantage. McKinsey B2B Pulse 2024.

BIM raises the stakes. When your product has a simple, accurate BIM family with embedded metadata (manufacturer, dimensions, performance, certifications, and link to the product page), it can be selected at design and pulled automatically into takeoffs and POs. BuildingSMART Canada’s ongoing initiatives and Ontario’s push on digital delivery signal where public and private projects are headed. Infrastructure agencies are investing in digital models and BIM‑to‑FM standards, which will cascade into contractor expectations on submittals and data quality. This is practical BIM technology adoption, not theory. buildingSMART Canada initiatives. Ontario digital delivery signals.

Threats are real. Large B2B platforms and national distributors keep improving punchout and API integrations. Local players like Copp’s Buildall already run searchable catalogues, which conditions London contractors to expect digital clarity at 10 p.m., not just at the counter at 7 a.m. On the opportunity side, EV‑manufacturing investment in nearby St. Thomas is drawing supplier ecosystems into the region, raising the premium on reliable, spec‑grade materials and documentation for industrial and commercial work. That pull can benefit nimble independents who publish product data and integrate lightweight order flows. The EV manufacturing impact is already altering regional procurement patterns. Ontario–Volkswagen St. Thomas investment.

Here’s a simple digital‑readiness ladder you can align to sales goals:

| Integration level | What it includes | Effort required | Expected near‑term benefit |

|---|---|---|---|

| Minimal | Accurate product pages with downloadable datasheets and EPD/HPD links | Low | Fewer submittal delays, higher phone‑to‑order conversion |

| Basic | 1–2 BIM families for top sustainable SKUs, searchable catalogue with stock status | Low–Medium | Spec mentions increase, faster reorders |

| Intermediate | Contractor login with contract pricing, saved lists, credit terms; punchout to common procurement tools | Medium | Higher repeat‑order rate, reduced quote friction |

| Advanced | API inventory/price feeds, model‑linked submittal generator, job‑pack kitting rules | Medium–High | Bid preference from specifiers, measurable margin lift on targeted lines |

Want to pressure‑test where competitors already perform? Re‑run the checklist from [how to identify your real competitors] against “digital clarity” and “spec data completeness.”

5. Practical playbook for independent suppliers: inventory, partnerships, digital steps and KPIs

Start with inventory you can defend. Curate 3–5 sustainable, code‑relevant SKUs in categories with frequent inspections: insulation, fenestration, sealants, MEP components. Build “spec packs” that

Mitchell Ozmun

SMB Researcher, Business Analyst - Saskatchewan Born and Raised