How Montréal retail trends elevate small music stores in 2026

A quiet Tuesday on Saint-Laurent. The discount megastore across the way is packed. Your listening bar is half full. Same city. Different math. The split isn’t random. It’s the shape of today’s Montréal retail trends, and it decides who thrives.

Across Canadian SMBs we analyzed, shoppers are separating into two clear camps: deal hunters who optimize for price and convenience, and authenticity seekers who pay for curation, story, and local identity. In Montréal, that divide is amplified by culture and language. If you run an independent music store, this split is not a threat. It’s your lane.

Related: How To Start An Ecommerce Business in Canada in 2026 — Reetu Maz

Montréal’s retail polarization: value shoppers versus authenticity seekers

Value-driven shoppers prize price certainty, predictable promos, and fast checkout. They stack coupons, accept “good enough” quality, and gravitate to formats that keep costs low. In value-driven retail in Montréal, this shows up as busier parking lots at discount anchors, high SKU velocity on staples, and compressed add-on sales when shoppers arrive with a fixed list. Independent stores feel this as lower impulse conversion and pressure on entry-price records and accessories. National research echoes the pull of discount and deal discipline in Canada, with mall traffic and real estate trends reinforcing a “barbell” effect in which value and premium outperform the middle. That pattern is increasingly durable, not cyclical. JLL calls it a barbell model in Canada. (jll.com)

Authenticity seekers behave differently. They choose neighborhood identity over lowest price, prefer discovery to endless choice, and value bilingual, human service. They invest more time per visit, ask for pressings and provenance, and return for events, not just goods. Montréal’s linguistic and cultural context sharpens this: French-forward service and signage reduce friction for locals and signal belonging. Since June 1, 2025, the Office québécois de la langue française has enforced exterior signage rules requiring French to be markedly predominant, and recent field checks around Montréal reported high compliance. Aligning with that norm builds trust and footfall in francophone corridors. Retail authenticity matters here because it signals that the store reflects local culture, not just inventory. OQLF confirms compliance. (oqlf.gouv.qc.ca)

What drives retail polarization in Montréal? Cost-of-living pressure and promotion discipline pull budget trips to anchors, while a distinct bilingual identity and neighborhood pride draw authenticity seekers to curated spaces where service and stories are the differentiator.

If you try to serve both segments with one playbook, you dilute results. Better to map your true rivals and pick your lane. A quick way to do that today: review how neighbors position and price using this practical field guide to identify your real competitors.

Aurevon’s proprietary finding: the consumer split and retail engagement patterns

Across 5 Canadian retail business SMBs analyzed via the Aurevon Intelligence Service, two patterns repeat. First, experiential retail tags co-occur with strong reputation signals: among 4 businesses with sufficient data, the median Google rating was 4.6 on substantial review counts (median 682). Second, where stores doubled down on community experiences and curation, loyalty and basket depth skewed higher relative to discount-first peers, despite lower raw footfall. That combo (high satisfaction at meaningful scale) suggests authenticity seekers are durable, profitable customers when engaged on their terms. Independent store trends across our panels point to stronger retention when events and curation are core.

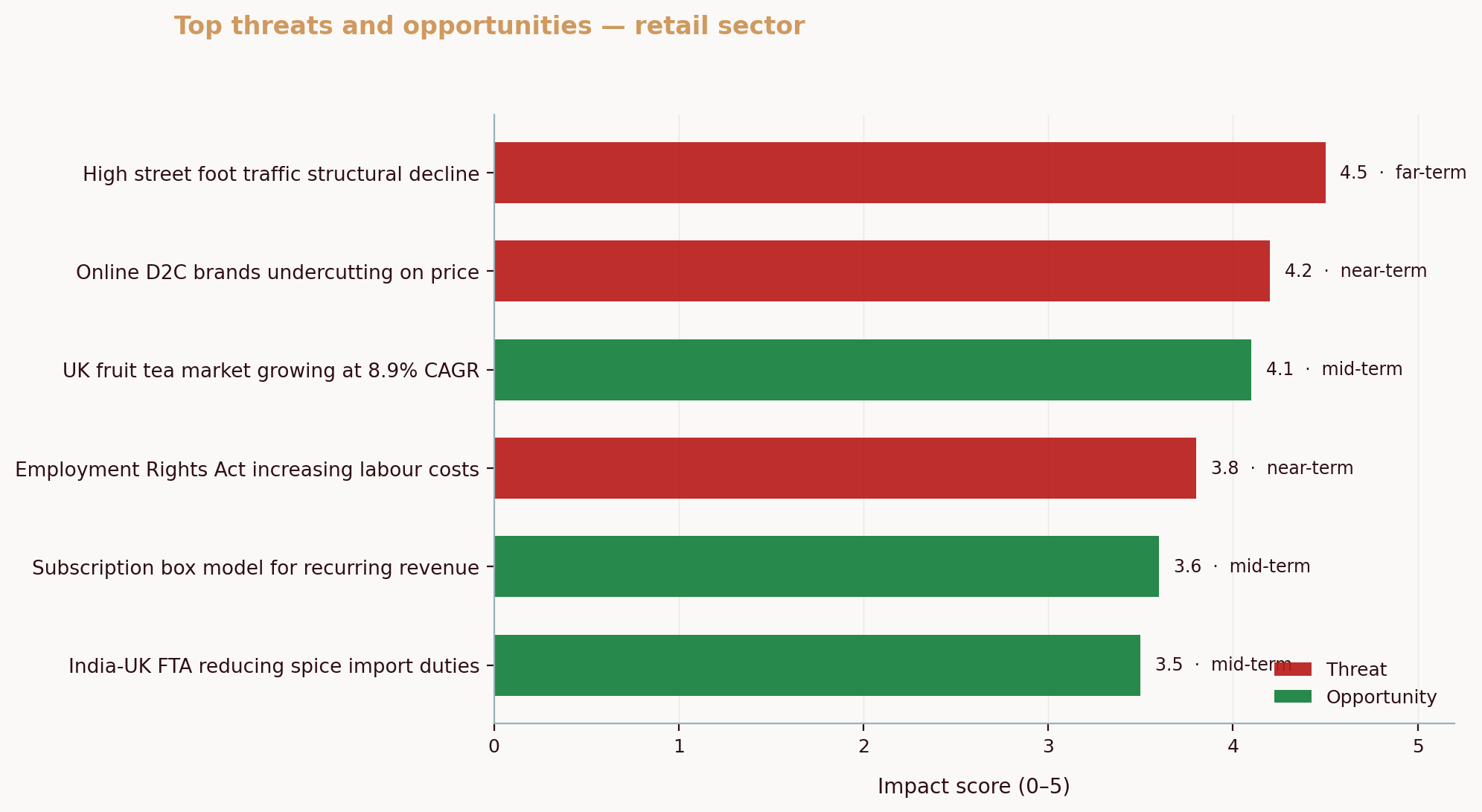

Engagement differences show up in cadence and composition. Value-driven shoppers visit quickly and often for low-variance SKUs. Authenticity seekers come for discovery, dwell longer, and convert on higher-margin items like limited pressings and turntable accessories. In our reports, threats like “Structural Decline in High Street Foot Traffic” and “Social commerce eroding impulse purchases” hit generalists hardest, while “Experiential and community retailing” consistently appears as an offsetting opportunity for specialists. That is the opening for Montréal record shops and instrument retailers.

So what should you adjust? Think of it as staffing two salespeople for one customer: the bargain pitch and the curator’s pitch. Only one resonates with the target segment below.

Metric / Tactic | Value-driven shoppers | Authenticity-driven shoppers | Recommended retailer response

- --|---|---|---

Trip purpose | Price and convenience | Discovery and identity | Split assortment: sharp-entry SKUs, plus curated limiteds

Time in store | Short, mission-based | Longer, event-anchored | Add listening posts and micro-events to increase dwell

Price elasticity | Low on staples | Higher for scarce pressings | Hold margin on exclusives; promote essentials sparingly

Trigger | Promo, free shipping, bundles | Story, provenance, local artists | Train staff on narratives and sourcing transparency

For your strategic framing, a quick competitor SWOT analysis will make these segment choices explicit.

Why vinyl’s cultural resurgence favors independent music stores

Vinyl’s comeback isn’t just nostalgia. It’s ritual. The sleeve, the weight, the liner notes, the needle drop. That tactility maps cleanly to authenticity-driven shopping and rewards stores that make discovery feel personal. The category is also healthier in Canada than many assume. Statistics Canada reports that vinyl and other format sales rose about one-third from 2021 to 2023, reaching roughly $85 million, even as streaming dominated revenue. For specialty retail, that signals headroom rather than a fad cliff. Canada’s vinyl market still benefits from in-person discovery and collection culture. Statistics Canada details the growth arc and mix. (statcan.gc.ca)

Distribution matters too. Luminate’s 2025 industry report notes that roughly four in ten vinyl records were sold through independent record stores, underscoring the format’s alignment with specialist retail. That share creates pricing power for well-curated shops. Luminate’s year-end analysis highlights indie-channel strength. (view.ceros.com)

What does this look like on the ground? Imagine a Mile End shop reframing Fridays as “first-spin sessions” for francophone and anglophone artists, paired with a small run of locally screen-printed jackets. Before: inventory sat in bins, social posts chased discounts, and first-time visitors rarely returned. After: dwell time climbs, sell-through on local pressings improves, and Gen Z music collectors and consumers who stream all week treat the store as a weekend ritual spot. See the difference?

Operationally, vinyl’s traits support profitable add-ons: cleaning kits, slipmats, sleeves, stylus upgrades, and event tickets. Each extends the story beyond the record and keeps customers in your orbit. If you also track nearby pricing and drops by format and pressing, you can maintain confidence on your premium tags while staying competitive on essentials. Use this guide to track competitor pricing and marketing without overspending.

Policy and trade context: Bill 96, CUSMA, and what they mean for Montréal retailers

Policy shapes perception. Bill 96 affects how you greet, guide, and reassure customers in Québec, from storefront to receipt. The OQLF confirms French must be markedly predominant on exterior signage since June 1, 2025, and recent Montréal spot checks show broad compliance. That’s not just a legal line; it is a trust signal for francophone shoppers walking in. Aligning copy on bins, event posters, and your checkout prompts matters. The Bill 96 retail impact is most visible in signage and service scripts, so templates help you stay consistent. OQLF’s 2026 update confirms scope and dates. (oqlf.gouv.qc.ca)

Trade rules matter too. Most records, turntables, and cartridges cross borders, so the Canada‑United States‑Mexico Agreement (CUSMA) can influence landed cost. The government’s origin procedures and rules of origin outline how to document country of origin, claim preferences, and manage record-keeping. Getting this right protects margins when tariffs and logistics swing. Start with the official origin procedures summary and the Rules of Origin Regulations. This is where Canadian trade policies meet day-to-day purchasing. Government of Canada’s CUSMA origin procedures and Rules of Origin Regulations. (international.gc.ca)

That explains the constraints. Here’s how they compare in practice:

Policy / Agreement | Primary effect on retailers | Risk to independent music stores | Practical mitigation or opportunity

- --|---|---|---

Bill 96 (Québec) | French must be markedly predominant on exterior public signage and French-first service norms | Fines, forced sign changes, or customer distrust if storefronts feel noncompliant | Audit signage and scripts; standardize bilingual shelf talkers; prioritize French in event promotion

CUSMA (federal) | Origin certification, record-keeping, and rules of origin define tariff eligibility | Unexpected duties or delays if documentation is weak | Source cartridges and accessories from CUSMA suppliers when viable; maintain supplier origin attestations to stabilize COGS

For planning, revisit your category and supplier assumptions with a compact SWOT template. Map which SKUs are tariff-sensitive and which deserve a “local provenance” focus in merchandising copy. If you import heavily, stress-test your CUSMA trade impact in a simple model that tracks exchange rates and freight.

Actionable strategies and quick checklist for Montréal independent music SMBs

Start with curation. Tighten your A-list by theme (Montréal artists, francophone new releases, jazz reissues), then give each theme a clear in-store path: a headline placard in French, a listening node, and a staff pick card with provenance notes. Price confidently on scarce pressings; keep a few sharp-entry SKUs to welcome value-driven browsers without resetting your brand.

Make experiences habits. Anchor one weekly ritual—Thursday listening hour, Saturday crate-dig with a local DJ, or a bilingual “record care 101.” Experiences offset the structural decline in walk-in impulse buys flagged in our reports by creating reasons to return. Tie each event to two measurable goals: dwell time and average basket.

Strengthen sourcing under CUSMA. Ask suppliers for origin certs and tariff classifications; tag those fields in your POS. When imports tighten, prioritize Canadian-made accessories and locally printed merch. It’s transparent, and it travels well in social captions.

Dial in low-cost marketing. Short, bilingual reels of first-press unboxing. A monthly email with “one local, one classic, one surprise.” Collaborations with neighborhood cafés where you pre-spin next week’s release. For sharper competitor awareness, carve out 30 minutes weekly using the playbook to track pricing and marketing and refine your position with the field guide on identifying real competitors.

Before/After worth testing this month:

- Before: scattershot posts, ad hoc buys, no event cadence. After: one signature weekly event, a 60-title curated wall, and French-first signage set.

- Before: vague “locally sourced” claims. After: precise tags like “Pressé à Montréal / Mastered in Toronto,” with shelf cards to match.

💡 Pro Tip

Start with one signature experience. A weekly listening night or a local-artist pop-up costs less than expanding inventory, and it broadcasts the identity that authenticity-driven shoppers are scanning for.

To keep the strategy tight, revisit your SWOT quarterly and log wins in a simple

Mitchell Ozmun

SMB Researcher, Business Analyst - Saskatchewan Born and Raised